Bartels Test vs Monte Carlo Simulation for Cycle Validation

Two approaches to answering the same question: is this cycle real or noise? When to use parametric testing versus simulation.

About this content: This page describes observable market structure through the Fractal Cycles framework. It does not provide forecasts, recommendations, or trading instructions.

Most articles on this site do not include static screenshots. Instead, we encourage you to run a free analysis on the platform to see exactly what is being described, with live, interactive results.

Bartels test vs Monte Carlo simulation are two methods for answering the same critical question in cycle analysis: is a detected cycle genuine or could it arise from random data? The Bartels test is a parametric method that calculates phase consistency probability, producing a 0 to 100% significance score in milliseconds. Monte Carlo simulation is a non-parametric method that shuffles data thousands of times to build an empirical null distribution, requiring more computation but making fewer statistical assumptions. In most cases both methods agree; when they diverge, the more conservative result is typically safer.

The Bartels Test Approach

The Bartels test is a parametric method that calculates the probability of observing the detected cycle phase consistency by chance:

- Divide data into cycle-length segments

- Measure consistency of returns at each phase point

- Calculate probability based on statistical distribution

- Report as Bartels significance score (0-100%)

Advantages: Fast computation, well-defined statistical properties, easy to interpret, no random seed issues.

Disadvantages: Assumes specific statistical properties that may not hold for all markets or conditions.

The Monte Carlo Approach

Monte Carlo simulation is a non-parametric method that estimates significance empirically:

- Detect cycles in actual data, note the power/significance

- Shuffle the data randomly (breaking any real patterns)

- Detect cycles in shuffled data

- Repeat many times (1000+) to build null distribution

- Compare actual result to null distribution

Advantages: Makes fewer statistical assumptions, can handle non-standard distributions, intuitive interpretation.

Disadvantages: Computationally expensive, results vary slightly between runs, requires careful shuffle method selection.

When to Use Bartels

- Real-time or near-real-time analysis (speed matters)

- Scanning many instruments (computational efficiency)

- Data reasonably approximates normal or symmetric distribution

- You need consistent, reproducible results

Bartels is the workhorse for production cycle detection systems.

Detect hidden cycles in any market

See which cycle periods are statistically significant in any market data — run a free analysis with our robust cycle detection software.

Try it free NowWhen to Use Monte Carlo

- Unusual or heavy-tailed distributions

- Research and validation (thoroughness over speed)

- Double-checking Bartels results on important decisions

- When you suspect parametric assumptions may fail

Monte Carlo is the robust fallback when you cannot trust parametric assumptions.

Practical Comparison

In most cases, Bartels and Monte Carlo give similar conclusions. If both say a cycle is significant (or both say it is not), you can be confident in the result.

Disagreements are informative:

- Bartels says significant, Monte Carlo says not: May indicate distribution issues; trust Monte Carlo

- Monte Carlo says significant, Bartels says not: Rare; investigate data properties

When they disagree, the more conservative conclusion is usually safer.

Implementation Considerations

For Bartels: Standard implementation is straightforward. Ensure you have enough cycle instances (at least 5-10) for reliable statistics.

For Monte Carlo:

- Use enough iterations (1000+ minimum, 10000 for precision)

- Choose appropriate shuffle method (full random, block shuffle, phase randomization)

- Consider computational cost for large-scale applications

Hybrid Approach

A practical workflow:

- Use Bartels for initial screening (fast)

- Filter to cycles with Bartels > 50%

- Run Monte Carlo on the filtered set (thorough)

- Only trade cycles that pass both tests

This balances computational efficiency with statistical rigor.

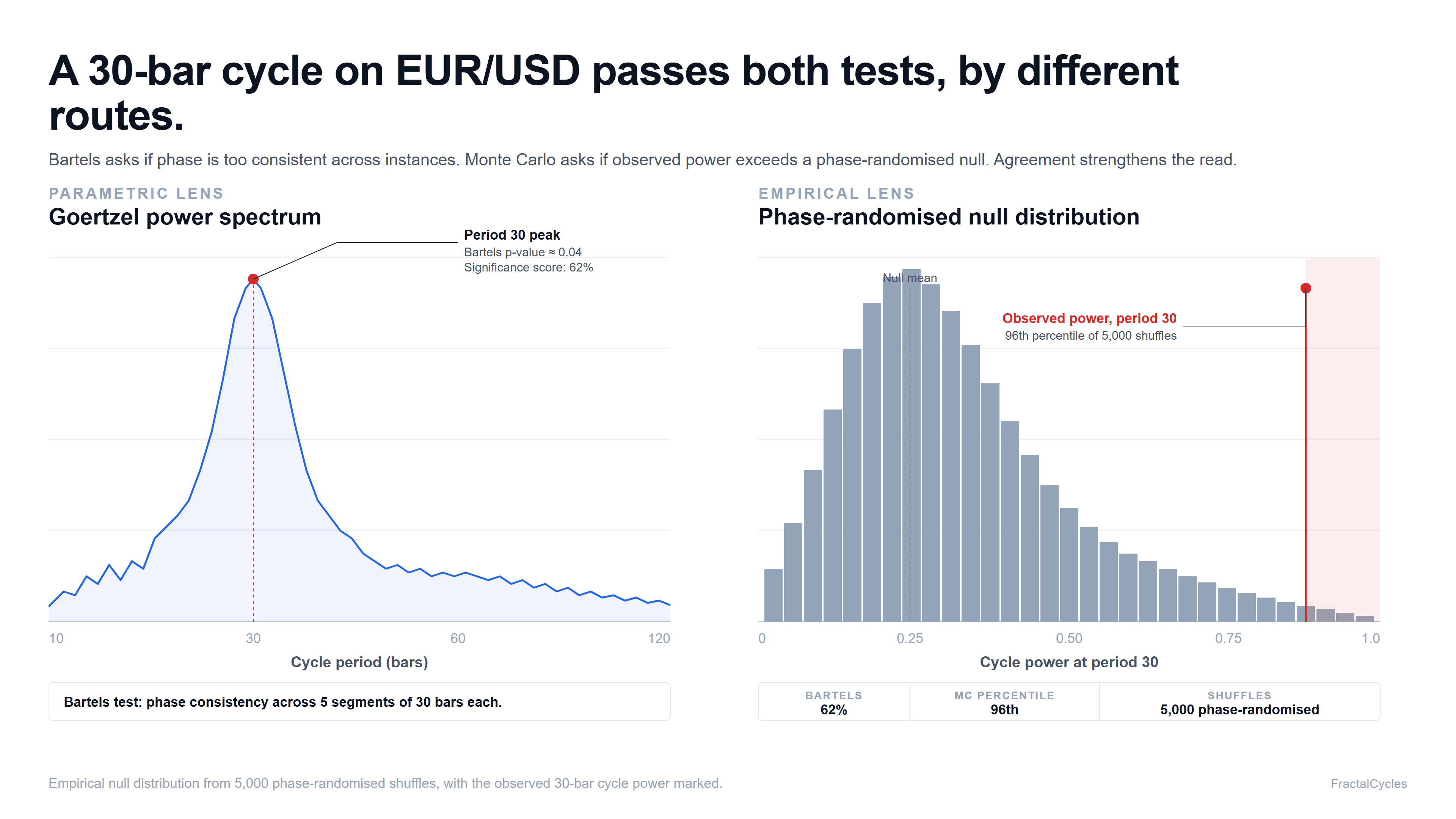

A Worked Example: 30-Bar Cycle on EUR/USD

Suppose an illustrative daily EUR/USD analysis over a four-year window flags a 30-bar cycle (roughly six trading weeks). The Bartels test, applied to phase consistency across the segments, returns a 62% significance score. To check the result with fewer assumptions, the same data is run through 5,000 phase-randomized Monte Carlo shuffles. The observed cycle power lands at the 96th percentile of the empirical null distribution.

The two methods agree, but they answer slightly different questions. Bartels asks whether the phase pattern looks too consistent across instances to come from independent draws. The phase-randomized Monte Carlo asks whether the spectral power at this period is unusually large given a shuffled version of the same series. Because phase randomization preserves the autocorrelation structure of returns, the test is conservative against spurious detections driven by smoothness alone. When both lenses point the same way, the cycle is meaningfully separated from noise on two independent counts.

The interesting case is partial agreement. If Bartels returned 62% but the Monte Carlo percentile sat near 70 rather than 96, the parametric assumptions might be flattering the result. Heavy-tailed return distributions, common in FX, can do this. The conservative read is to defer to the empirical test and treat the cycle as borderline. Readers who want the underlying mechanics can review Bartels significance testing and cycle validation, and the broader structural context appears on the EUR/USD market page.

Choosing a Shuffle Strategy

The Monte Carlo result is only as good as the null model it is built against. Three shuffle strategies dominate practice. Full random permutation destroys all temporal structure and is the strictest test, but it can be too easy to beat because real return series have autocorrelation that pure noise does not. Block shuffling preserves short-range dependence by reshuffling fixed-length blocks. It is appropriate when the cycle of interest is long compared to those blocks. Phase randomization in the frequency domain preserves the autocorrelation structure exactly while destroying phase relationships. That is usually the right null when the question is specifically about cyclic phase.

In production-style screening across many instruments, the choice of shuffle strategy matters more than the iteration count above the 1,000 mark. A well-chosen null with 1,000 iterations will routinely outperform a poorly chosen null with 10,000. Pair the shuffle with the question. If the question is "does this period have unusual power given typical autocorrelation," phase randomization is the natural match.

Our Approach

At FractalCycles, we use Bartels as the primary validation method for its speed and reproducibility. We apply Monte Carlo for research validation and when users want additional confirmation of important findings.

Framework: This analysis uses the Fractal Cycles Framework, which identifies market structure through spectral analysis rather than narrative explanation.

Written by Ken Nobak

Market analyst specializing in fractal cycle structure

Get the Monthly Market Cycle State Report

Free market cycle data for 20+ instruments. Dominant periods, regime shifts, and phase transitions delivered every month.

No spam. Unsubscribe anytime.

Disclaimer

This content is for educational purposes only and does not constitute financial, investment, or trading advice. Past performance does not guarantee future results. The analysis presented describes observable market structure and should not be interpreted as predictions, recommendations, or signals. Always conduct your own research and consult with qualified professionals before making trading decisions.

See cycles in your own data

Apply the Fractal Cycles framework to any market using our analysis tools. Start with a free account.